Roasted When You Order

Get 10% off and FREE shipping on your first coffee subscription order.

Use code “BREW” at checkout.

Shop Now

Get 10% off and FREE shipping on your first coffee subscription order.

Photo: ©fizkes from Getty Images via Canva.com

You may want to read:

Stewarding money is not only a privilege, but it’s a sober responsibility because of the temptations and snares that entangle too many of our brothers and sisters. The seductive nature of sin and the culture’s encroachments into our lives has caused many Christians to struggle to bring their finances under the Lordship of Christ. This matter is symptomatic of a deeper issue that needs addressing. The selfish use of money is a worship disorder of the heart, which is crucial intel we must understand when helping someone overcome fiscal irresponsibility.

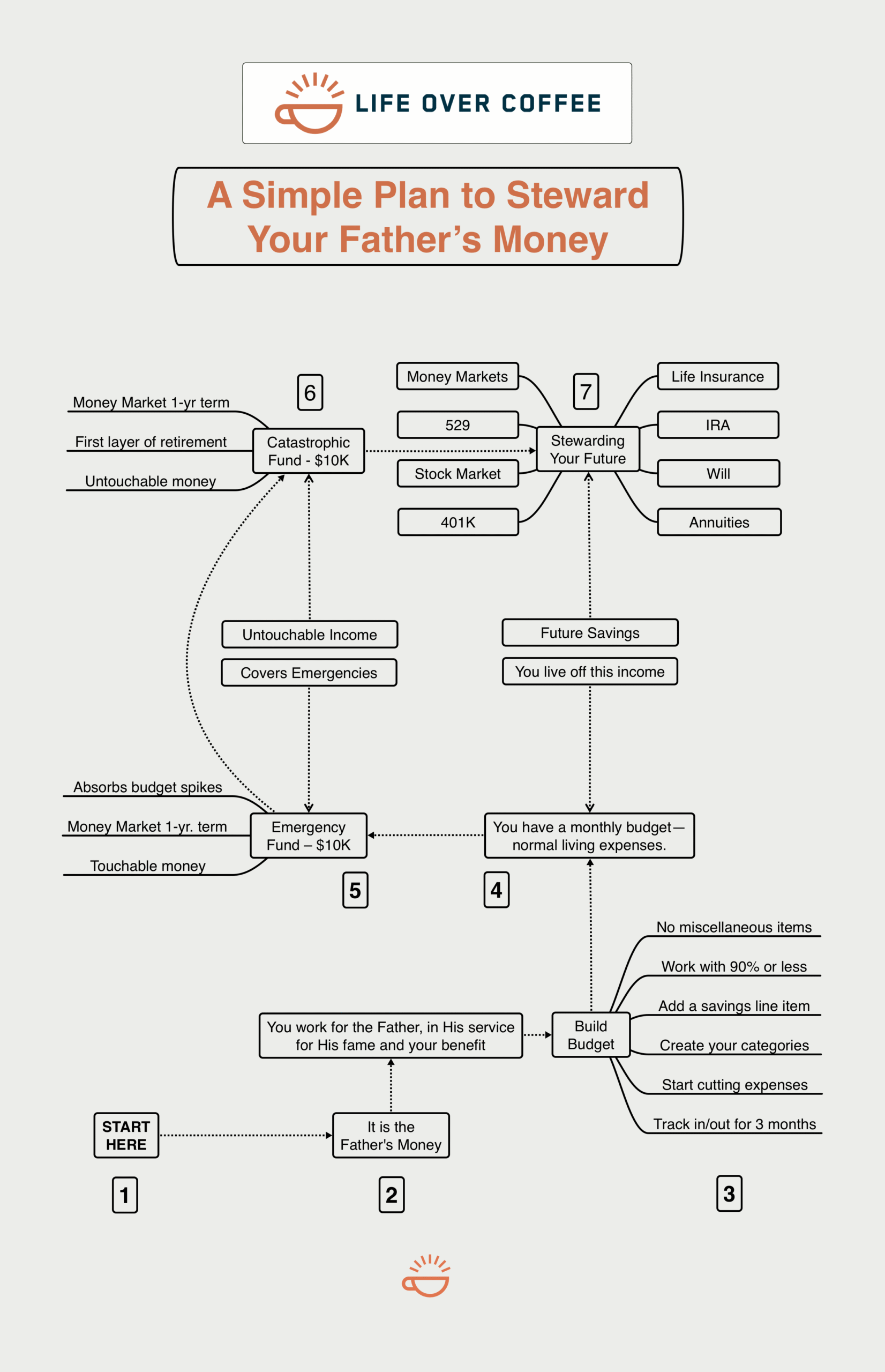

Money problems will not go away without putting off bad habits and renewing our hearts (Ephesians 4:22-23). So, yes, we must deal with the behavior because Jesus was clear that we are to cut off our hands if they are offensive (Matthew 5:30). Thus, we amputate behavioral sins while we mortify heart idolatries. Amputation speaks to what is external, while mortification speaks to the source or cause of our problems. However, in this chapter, I will interact with the external matters of money while appealing for you to find a mentor to help you address any heart idolatries that have led to fiscal irresponsibility. Below is a mind map to guide you through this chapter.

When I work with folks on their finances, the typical person does not see how their financial stewardship is a responsibility that should have God’s glory as primary—a typical response that motivated me to create this mind map. I recognize that there are many ways to steward the Lord’s money. What I am presenting to you is merely one of those ways. I am practicalizing common sense, not telling you that the Bible mandates you to follow this plan and pathway religiously. There is “a” way of doing things, and there is “the” way.

This exercise is suggestive; it’s one way for you to think about money. The mind map is a roadmap to give you inspiration and a vision that you will need to tweak and implement according to your season of life, the size of your family, your monetary situation, and your age. Though your plan may not be exactly like this plan, the big ideas in this mind map are universal. I hope that what you read will spur you to adapt these ideas to your life. Let’s take a look.

The first big idea is that our money is not our money. (See #1 in the mind map.) If we don’t start with this presupposition, we will not end with God’s glory in mind. Our beginning will determine our ending. If we fully believe every cent we have is God’s and it’s our job to steward those pennies, we have positioned our hearts in the right place as God’s Money Manager. When someone asks you about your role with your finances, you can tell them that you are a Money Manager for God. It’s a sobering job title, and there is not a pay grade higher than that one.

Lucia and I think about finances this way. We have never thought about the money we have as being ours; we’re stewards of what He gives. Perhaps prayer will assist in adopting this mindset. You could place a note on your bathroom mirror or refrigerator to help imprint this worldview into your psyche. As you fixate on this overarching truth, you’re ready to follow your King to financial maturity. The next step is doing His work on earth. (See #2 in the mind map.)

With steps one and two firmly under your theological belt, you’re ready to build a plan. (See #3 in the mind map.) This plan has passed the field test: Lucia and I have followed this financial process our entire marriage. However, the budget you create is your unique roadmap. If you don’t have a map, you will not know where you’re going. I have been doing financial counseling for many years, and I’ve never met a person who did not have a budget and knew where all the money went.

The counselee says, “Oh, I have a pretty good handle on our money. I know where it goes.” It’s always a lie, even an unwitting one; the person typically does not connect what he says to deceit. His response is nothing more than an attempt to soft-pedal his irresponsibility. At that juncture, I challenge him to make a budget. It’s a common-sense thing to do, but it does take diligence. A simple, albeit tedious, way to do this is to chart every cent you receive and spend for an entire month. You’d be amazed at some of the stories I have heard after folks did this.

They are always shocked at the amount of money they are spending. Most of the time, it’s on items like eating at restaurants. There are usually four to seven other categories that shock them. After collecting this data for a month, they become more concerned about how much they waste and are motivated by how much they could be saving. From the prior month’s worth of work, they begin developing categories or line items according to groupings of expenses. These line items become the categories from which they spend money each week, each month. Depending on how detailed they become, there could be as many as fifty of them. They can work from these line items for the rest of their lives.

The first time I went through this process was in the early ’90s. I had over 100 line items from my first month’s data collection. I trimmed that list to about forty groups. For example, I had three line items for food: grocery, eating out, and snacks. I did not have a line item for savings. Shockers! The goal is to work from 90 percent of your gross income. Though the New Testament does not teach giving 10 percent to the church, giving that amount is a good starting point (2 Corinthians 9:7).

You now have a good idea of how much comes in during the month and how much exits. You have also created most of the categories you will need. At this juncture, you start cutting back on your expenses and categories. (See #4 in the mind map.) Do not create a miscellaneous item because it could turn into a black hole, which is tempting for the person who has been irresponsible with money. The trimming part is usually fun, especially after seeing how the new budget has debt reduction and savings categories (Proverbs 22:7).

Some couples have turned this process into a financial game. The addictiveness to spending money shifts to an addiction to reduce debt and save money. I recommend that you continue to track your expenses with meticulous detail, at least for the first year. No one month is the same. Birthdays, Christmas, insurance payments, and other costs show up at different times during the year. If you track the entire year, you will have a clear idea of your expenses and income. You will also create special categories to put aside a certain amount each month, which will level out those one-time expenses like Christmas.

If you’re not in a position to start saving large amounts, don’t be discouraged. Begin with small, steady contributions. Even setting aside $10 or $20 a week creates momentum, a mindset shift toward stewardship. The goal isn’t instant perfection but progressive direction. The real victory is cultivating the discipline of delayed gratification and faithful management, which, over time, produces peace and resilience. And here’s something worth noting: saving money honors God because it reflects His character. God is a preparer, a planner, and a provider. He prepares a place for us (John 14:2). He plans the end from the beginning (Isaiah 46:10). He provides all we need according to His riches in Christ (Philippians 4:19). As you build an emergency fund, you mirror your Father’s foresight and care.

Untouchable money is not just a safety net for rare and catastrophic events but also a legacy fund. When you think in terms of legacy, you shift from merely surviving to long-term faithfulness. This money can eventually help children, bless missionaries, support church plants, or provide for aging parents. The Proverb reminds us, “A good man leaves an inheritance to his children’s children” (Proverbs 13:22). Imagine raising children who see you live within your means, save faithfully, and give generously. What kind of adults will they become? How many of our financial patterns are caught, not taught? If your children see you managing money with integrity, dependence on the Lord, and generosity, they will be inclined to imitate you. This untouchable fund, wisely grown over the years, will enable you to sow richly into the lives of others without instability or fear.

The future stewardship section (#7 in the mind map) focuses on long-range planning: college, retirement, and estate planning, but it must remain gospel-centered. Our future is not merely about comfort or accumulation. It’s about freedom to serve. For example, early financial discipline could position you for generous ministry in your 60s or 70s—perhaps traveling to equip churches, supporting global missions, or taking on part-time disciple-making roles. You can’t do that if debt crushes your flexibility. Good stewardship sets you free. It increases your availability to be used by the Lord in ways that reckless spending can never allow. And don’t overlook the importance of basic legal planning: a will, power of attorney, and life insurance—especially if you have dependents.

These tools are not fear-driven precautions but acts of love. It’s one more way to live out Philippians 2:4—looking not only to your own interests but also to the interests of others.

Remember this: no plan works without feedback. One of the greatest acts of humility in financial discipleship is inviting someone into your financial world. Invite a spiritually mature friend or mentor to sit down with you once a quarter or once a year to evaluate how you’re doing. Let them ask the hard questions. Let them see your budget, your giving, your debt, and your goals. “Faithful are the wounds of a friend.” Proverbs 27:6 tells us you’re not alone. And if you’ve been financially unfaithful for years, the good news of the gospel still applies. Jesus forgives. The Spirit empowers.

The church equips. You can repent, rebuild, and rejoice. But it starts with honesty. If you’ve never talked with your spouse about money openly, prayerfully consider doing so this week. Sit down together. Lay out everything. No shame. No blame. Just mutual repentance and redemptive action. If you’re single, consider asking a mentor or elder to walk with you. There is grace in community and wisdom among the godly.

You don’t have to be rich to be a faithful steward. You don’t need a six-figure salary to please the Lord. Stewardship is not measured by quantity but by quality. It’s not about how much you have but how you steward what you have. Let me leave you with this: Financial integrity is a gospel issue. When you bring your bank account under the Lordship of Christ, you reflect a heart that trusts Him deeply. You show that He is more precious than possessions. You resist the siren call of materialism. You choose contentment over consumerism, worship over worry, mission over mammon. So, take the next step. Use this mind map as your framework. Adapt it. Share it. Teach it. And most importantly, live it. Let your stewardship speak of your Savior.

Rick launched the Life Over Coffee global training network in 2008 to bring hope and help for you and others by creating resources that spark conversations for transformation. His primary responsibilities are resource creation and leadership development, which he does through speaking, writing, podcasting, and educating.

In 1990 he earned a BA in Theology and, in 1991, a BS in Education. In 1993, he received his ordination into Christian ministry, and in 2000 he graduated with an MA in Counseling from The Master’s University. In 2006 he was recognized as a Fellow of the Association of Certified Biblical Counselors (ACBC).